The Subplot

The Subplot | Huddersfield is the future of the UK’s regional policy. Here’s why.

Welcome to The Subplot, your monthly slice of commentary on the business and property market from across the North of England and North Wales.

This month’s long read

- The future begins tomorrow: take a peek into the ups and downs of the next few years of regional policy with a trip to Huddersfield, West Yorkshire’s potential wonderland.

- Elevator pitch: your guide to what’s going up, and what’s heading the other way

WEST YORKSHIRE’S WONDERLAND

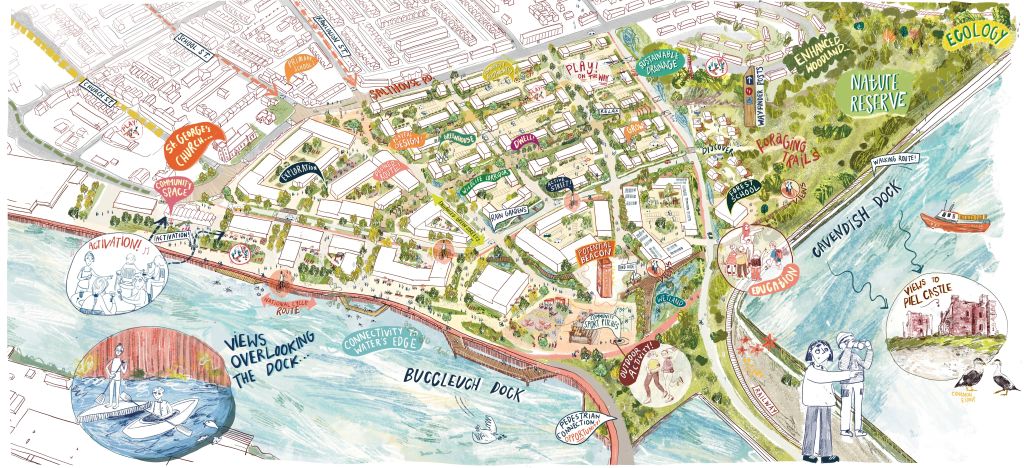

Huddersfield, gateway to the future

The future of regional policy is already on show for those who want to see it, and it’s in Huddersfield. And it’s all about connectivity – not so much planning reform or Green Belt.

Will a Keir Starmer government be able to learn the lesson here for Northern economic growth?

Something is going on in and around Huddersfield, and it’s wonderful: economic growth, and lots of it. Research by the Northern Powerhouse Partnership shows economic output per hour worked soaring in Huddersfield and its hinterland in a way it doesn’t anywhere else in West Yorkshire – and hardly anywhere else in the North.

Numbers to know

The figures speak for themselves. Between 2004 and 2022, GDP per hour worked in Kirklees and Calderdale rose by 25.7%. That’s under the 33.7% recorded in powerhouse Manchester (city, not city region). Yet it is miles ahead of almost everyone else nearby. For comparison, Bradford was 17%, Leeds scored 11%, and Wakefield had a struggle to reach 2%.

Special location

Why the surge? The answer is another number: there are currently only 10,000 working people in the North who can get to the region’s four big cities, and Manchester Airport, in less than an hour. They all live in or around Huddersfield. Moreover, the idea of becoming one of those 10,000 or so is very appealing to urbanites from Manchester and Leeds. Font Comms boss Rebecca Eatwell is one of them. She moved from Chorlton to Huddersfield’s rail-served hinterland in 2019. In her village, emigrée Mancunians and Leeds-dwellers are behind a fancy new kids’ shop, a smart diner, and plenty else.

City exodus

“I wouldn’t have moved here unless they’d opened up the train line from my village. In the last five years, more people from Manchester and Leeds have started to move to the rural communities surrounding Huddersfield, attracted by the easy commute into either city. Whilst the town at the moment feels pretty unloved, it’s got huge potential, and if some of the regeneration projects mooted in the 10-year blueprint come off it could become West Yorkshire’s next go-to destination,” says Eatwell.

It’s all about connections

In other words, Huddersfield’s economic growth has got everything to do with connectivity, says Northern Powerhouse Partnership chief executive Henri Murison. “Huddersfield is like the canary in the coal mine for Northern Powerhouse Rail – because it shows that connectivity makes towns more prosperous.” He has commissioned further research to prove the point. “If you could only do one thing to boost regional growth, then you would improve connectivity. Lack of it is a binding constraint, it’s one of the key reasons the North is less productive than the South,” he insists.

But, money

Is a potential Labour government promising the surge of infrastructure investment this implies? Not precisely. The manifesto says a Labour government will develop “a 10-year infrastructure strategy, aligned with our industrial strategy and regional development priorities, including improving rail connectivity across the North of England. The strategy will guide investment plans and give the private sector certainty about the project pipeline. We will work closely with business to map and address the delivery challenges we face. We will create a new National Infrastructure and Service Transformation Authority, bringing together existing bodies, to set strategic infrastructure priorities and oversee the design, scope, and delivery of projects.” Cynics note that this is mostly about writing something, delivery is at the end of the list, and no funding is promised.

Commuters are super

In Labour-run Kirklees most of those leading regeneration are inclined to see the best in the manifesto’s promises. But they nonetheless insist that better transport infrastructure means more growth. Those relocators include commuters – once regarded with some hesitation, but now whole-heartedly embraced. Huddersfield Unlimited chair (and former Kirklees Council Leader) Sir John Harman, says: “There was once a question about whether we wanted to grow our commuter hinterland, but with working from home there’s no longer a choice between wealth creation and commuting economies. It’s a false choice. We can do both. Huddersfield means access to the big cities, so economic development is now a very residential property thing.” Along with connectivity, Sir John suggests some weekend-and-evening cultural assets – restaurants, entertainment – would help cement the town’s reputation as a West Yorkshire wonderland.

Plans afoot

Kirklees Council already has that cultural-and-lifestyle problem in hand, part of what’s badged as a £1bn investment. In June last year, Kirklees Council selected BAM to deliver the first phase of Our Cultural Heart, a comprehensive revamp of Huddersfield town centre.

The project involves the refurbishment of the former Queensgate Market and Huddersfield Library buildings to house a food hall – inevitably described as ‘vibrant’ – and a modern museum and gallery. In March this year, the council allocated £16.7m of Levelling Up Funds, and accepted a further £48m for the Penistone rail line upgrade. Another £20m for Dewsbury – which has Huddersfield’s locational advantages but not yet the economic payback – and £17m for an investment zone. This is big stuff.

But money, again

Will there be more dosh? Unless we’ve all been seriously deceived, potential chancellor Rachel Reeves will not unveil a torrent of infrastructure spending in her autumn budget. But will she maintain the existing regime of investment zones, enterprise zones, and levelling-up funding? Says Sir John: “The risk is to the investment planned as a lever for growth. That it’s pretty well committed, but were it to suddenly evaporate… I don’t think the upgrade to the TransPennine rail link will evaporate, that’s baked in, but if investment zones or levelling up spending were to be hacked back or change direction… I don’t think we’d lose the whole game in Huddersfield, but we’d lose momentum. So it’s important we learn from the new government that those plans are still in place. I hope so, but one never knows.”

Heard this before

If Labour is successful, Keir Starmer and Reeves have already said there will be an announcement from Angela Rayner on planning reform and Green Belt within the month. Will this kickstart growth in the way infrastructure spending might? Possibly not. It’s not unwelcome but it’s not setting hearts racing, either. Henri Murison says that improving connectivity opens up more sites for housing. “The North’s problem isn’t so much that you can’t get a decent house at a reasonable price, but that wages are below average in places that aren’t well connected.”

Land questions

Huddersfield might benefit from additional land – it’s hard to say. A 2020 employment land review wasn’t published, but the 2019 version was: small pockets south of Huddersfield add up to little, and the town itself had 98 acres. A 2023 report suggested Kirklees was using up employment land at roughly the rate it was being provided. But bear in mind that most of the commercially interesting logistics sites are north of the town in Calderdale borough. Housing land is also running a little short: a May 2024 report suggests that a five-year land supply has dropped to a 3.96-year supply. Not a crisis, but a move in the wrong direction. The problem is topography: large flat sites are rare. Calderdale has agreed two large urban extensions that will do some of the work, and developers are said to have plenty of extra options up their sleeves.

The outcome? Savills development director Simon Douglas says: “It’s not either or. Huddersfield needs both the infrastructure and the land.” By this time tomorrow, we’ll probably have a new government. The unusually rapid pace of growth in Huddersfield ought to attract its attention. Very soon we’ll find out if it has.

E LEVATOR PITCH

LEVATOR PITCH

What’s going up, and what’s going down

Some sources of property lending begin to look a bit fragile, while investor interest in the big shed sector perks up

a little. A confusing summer ahead? Doors closing.

Paying the price

Paying the price

As the Greater Manchester Combined Authority prepares to defend its decision to allocate £508m of its £942.5m housing investment fund to Renaker – a case before the Competition Appeals Tribunal is pending – spare a thought for other property lenders with a looming headache. Then pause to consider how much pain this could mean for Northern real estate, and people like you.

The mood isn’t brilliant: deals take forever, funders are hesitant, the property market is sticky and samey. It’s 2023 all over again.

The total volume of lending to commercial property has fallen off a cliff – it hasn’t been this low since 2013. At the same time about £71bn of the roughly £170bn of loans outstanding will have to be refinanced within 12 months, says Bayes Business School. A credit famine + urgent need to refinance = distress.

So far, private equity has stepped in when others have pulled back, accounting for about 20% of commercial property lending. But that’s not necessarily a good thing. Last week’s Bank of England Financial Stability report, says PE’s high leverage, fuzzy valuations, and “strong interactions with riskier credit markets” pose a risk, which could spill over into other parts of the finance sector, and could be exaggerated from spill over from turmoil in the (much wobblier) US private equity sector.

Lately, PE has swerved away from commercial, opting instead for city living: Singapore-based Q Investment Partners at Merrion Street in Leeds, or Cain International at First Street in Manchester. But the commercial sector hasn’t been abandoned – oh no. The largest recent PE buy was New York-based private equity giant KKR buying shed plots at Omega Warrington and before that the unexpected arrival of Luxembourg-based Parthena Reys, which is believed to have paid something north of £70m for the office block at One Hardman Boulevard in Manchester.

If you think interest rates aren’t going to drop soon, and that the UK’s ballooning public sector debt isn’t going to let it drop very far – remember Liz Truss and the bond markets – then the gradual ratcheting up of private equity risk seems unavoidable. Without the liquidity private equity helps to provide it’s going to be hard to get much built – regardless of whoever sits in 10 Downing Street.

Seizing the (muddled) day

Seizing the (muddled) day

Tuesday morning saw two announcements, one from Barings and one from Panattoni, both announcing the purchase of a 65-acre site on the A1(M) and neither mentioning the other. By studying the pictures you could work out that they were talking about the same site. Enquiries later revealed the buy was funded by the former, to be developed by the latter.

This splendid media cock-up heralds what is trumpeted as the North’s largest speculative development in the form of a 770,000 sq ft building on a site consented for 1.2m sq ft. Work is due for completion by September next year.

The confusion is emblematic of a funny, unsettled industrial scene. Cushman & Wakefield data shows investors are abandoning the shed sector: Q1 2024 data showed investment volumes down 35% on the five-year average. When investors decide to splurge it tends to be modest (meaning under £50m). Take-up is down 12% on the fairly poor showing of late 2023.

So why buy the Junction 34 site today? There might, just might, be a few decimal points of yield gap to exploit between the North and the South. But the story is nabbing a slice of a location that occupiers love, in a market that (by late 2025) could be running out of the new big boxes they also love. Known demand is beginning to creep back up – nothing to get giddy about, but at 4.7m sq ft it’s the highest it has been for 18 months. Meanwhile, supply is edging down with the stock of available sheds nudged below by 3% in the first quarter. Investor activity is relatively more visible in the North than in the trickier South.

The real winner here is vendor Mulberry Developments, which picked a lovely hope-filled moment to unload a good quality plot. As summer turns to autumn the mood might not be so bright.

Get in touch with David Thame: [email protected]